If your business sells to other businesses, you’ve likely felt the pain of waiting 60 days for a payment that should have come in at 30. That gap, between the moment a customer places an order and the moment cash actually lands in your account, is exactly what the order to cash process is designed to close.

Also written as O2C or OTC, the order to cash business process is one of the most consequential workflows in any B2B operation. When it runs smoothly, your cash flow is predictable, your customers stay happy, and your finance team isn’t buried in follow-up emails. When it doesn’t, even a profitable business can find itself cash-strapped.

This guide breaks down what the order to cash process actually involves, where it tends to break down in B2B payments, and what it takes to fix it.

What Does Order to Cash Mean, and Why Does It Matter?

The order to cash process covers every step between a customer placing an order and your company successfully collecting payment for it. That includes order processing, credit checks, fulfillment, invoicing, payment collection, and cash application.

It sounds straightforward. In practice, especially in B2B environments, each of those steps involves its own team, its own system, and its own set of risks.

The reason the O2C process matters so much is its direct connection to cash flow. Every delay, whether in fulfillment, invoicing, or collections, means money that should be working for your business is instead sitting in someone else’s accounts payable queue. For businesses operating on tight margins or with large customer orders, that wait time can create real financial pressure.

In B2B payments specifically, the order to cash process flow is also more complex than in consumer transactions. Orders are larger. Payment terms stretch from 30 to 90 days. There are often multiple stakeholders involved in approving invoices on the customer side. And disputes, when they happen, take longer to resolve. All of this makes a well-structured O2C cycle essential, not optional.

O2C doesn’t operate in isolation either. It works alongside Procure-to-Pay (P2P) and Record-to-Report (R2R) as one of three core cycles that together run your entire finance function.

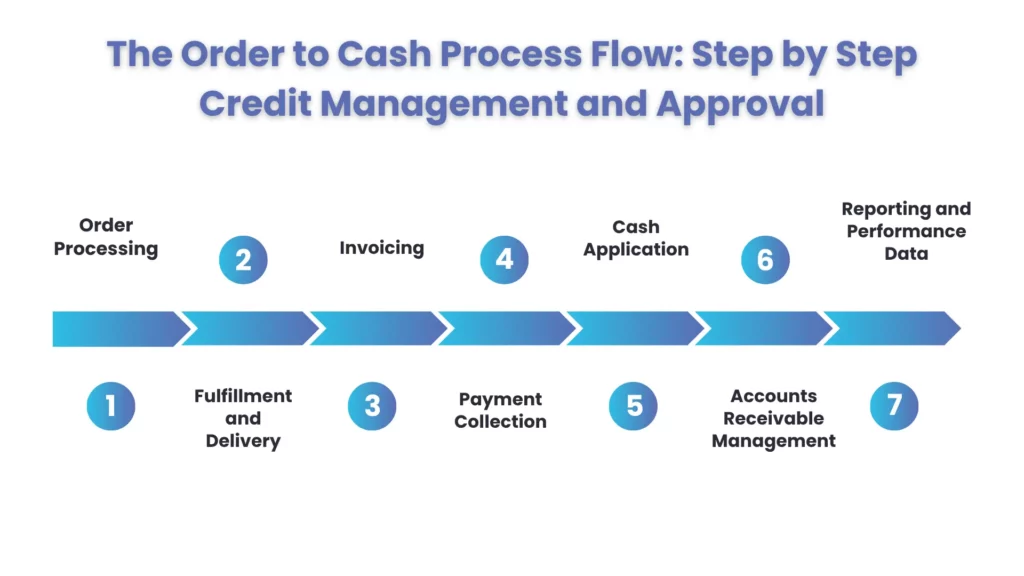

The Order to Cash Process Flow: Step by Step

Understanding the business process order to cash means understanding what happens at each stage and where things can go wrong.

Step 1: Credit Management and Approval

The O2C cycle starts before a single order is placed. If you extend credit to a customer, which most B2B relationships involve, you need to assess whether that customer is likely to pay, and on what terms.

This means running credit checks, reviewing payment history, and setting appropriate credit limits. Done well, this step filters out high-risk accounts before they create collection problems downstream. Done poorly, or skipped entirely, you end up chasing payments from customers who were always unlikely to pay on time.

The Federal Trade Commission’s guidelines on business credit practices provide a useful baseline for understanding your legal obligations when extending credit to commercial customers.

A fast, structured credit approval workflow doesn’t just reduce risk. It also speeds up the overall order to cash process by making sure orders from creditworthy customers can move forward without delays.

Step 2: Order Processing

Once a customer places an order, it needs to be accurately entered into your order management system, verified against available inventory or capacity, and moved into the fulfillment queue. Any error here, wrong quantity, wrong product, wrong pricing, creates a ripple effect that delays invoicing and payment.

Clear order forms, trained staff, and wherever possible, automated data entry help keep this step clean. It’s also the right moment to confirm that payment terms are documented and agreed upon, so there are no surprises later in the O2C process.

Step 3: Fulfillment and Delivery

Whether you’re shipping physical goods or delivering a service, fulfillment is where the commitment to the customer becomes real. For product orders, that means picking, packing, and shipping accurately to the right address within the agreed timeframe. For service orders, it means coordinating delivery, scheduling, and ensuring that everything promised in the contract is delivered as specified.

Why does fulfillment matter within the order to cash process flow? Because you typically can’t issue an invoice, or expect payment, until the customer has received what they paid for. Slow or inaccurate fulfillment directly delays your cash inflows.

Step 4: Invoicing

Invoicing is where a lot of B2B finance teams lose time. An invoice that goes out late, contains errors, or doesn’t include the right information gives customers a reason, or an excuse, to delay payment.

A strong invoicing step in the end to end O2C transformation for B2B operations means getting accurate invoices out quickly after fulfillment, in a format the customer can process without confusion. The IRS guidelines on business recordkeeping and invoicing requirements set out what documentation US businesses are expected to maintain, and a compliant invoice structure satisfies those requirements while keeping your collections process clean.

Standardized templates, automated invoice generation, and digital delivery all reduce the friction here. The invoice is your formal request for payment. The faster and more accurately it goes out, the sooner your payment clock starts.

Step 5: Payment Collection

Payment terms in B2B payments commonly run Net 30, Net 60, or even Net 90. That means even a smooth, dispute-free transaction can take months to convert to cash. The payment collection step involves ensuring customers pay within agreed terms, and following up proactively when they don’t.

The types of payment methods you accept, the reminders you send, and the ease with which a customer can actually pay all influence how quickly this step completes. Businesses that make it easy to pay, through online portals, automated reminders, and multiple payment options, consistently see faster collections than those relying on paper checks and manual follow-up.

For US enterprises looking to reduce Days Sales Outstanding, AR automation is one of the highest-impact changes you can make to the payment collection step.

Step 6: Cash Application

Receiving payment is not the same as knowing you’ve been paid. Cash application is the process of matching incoming payments to the correct outstanding invoices and updating customer account balances accordingly.

This step sounds administrative, but it’s more complex than it looks. When customers pay multiple invoices in a single transfer without remittance advice, reconciliation becomes a manual puzzle. Errors in cash applications create false pictures of who still owes what, and can delay collections on invoices that were already paid.

Automating cash application, using remittance data where it’s available, and maintaining clean customer account records makes this step far less painful. For finance teams managing high payment volumes, this is also where cash flow management strategy and O2C execution directly intersect.

Step 7: Accounts Receivable Management

Not every payment arrives on time. When it doesn’t, the accounts receivable function steps in to recover what’s owed. This might involve sending payment reminders, calling customers to discuss overdue balances, setting up payment plans, escalating to a collections process, or resolving disputes about the invoice itself.

The key to managing AR well within the broader order to cash business process is visibility. If your system can’t tell you which invoices are overdue, by how much, and for which customers, you’re always reacting rather than managing. Good AR systems flag issues early, so your team can intervene before small delays become large write-offs.

It’s also worth noting that under the Fair Debt Collection Practices Act (FDCPA) administered by the CFPB, certain collection practices are regulated even in commercial contexts, understanding these boundaries keeps your collections process compliant and professional.

Step 8: Reporting and Performance Data

The final step of the O2C process is often the one most businesses underinvest in: actually measuring how the cycle is performing.

Days Sales Outstanding (DSO), invoice accuracy rates, time-to-collect by customer segment, dispute frequency, these metrics tell you where your order to cash process is working and where it isn’t. Finance teams that track this data can spot patterns: a particular customer who consistently pays late, an invoicing error that keeps recurring, or a fulfillment delay that’s triggering disputes.

Without data, you’re optimizing blind. With it, you can make targeted improvements that have a measurable impact on cash flow.

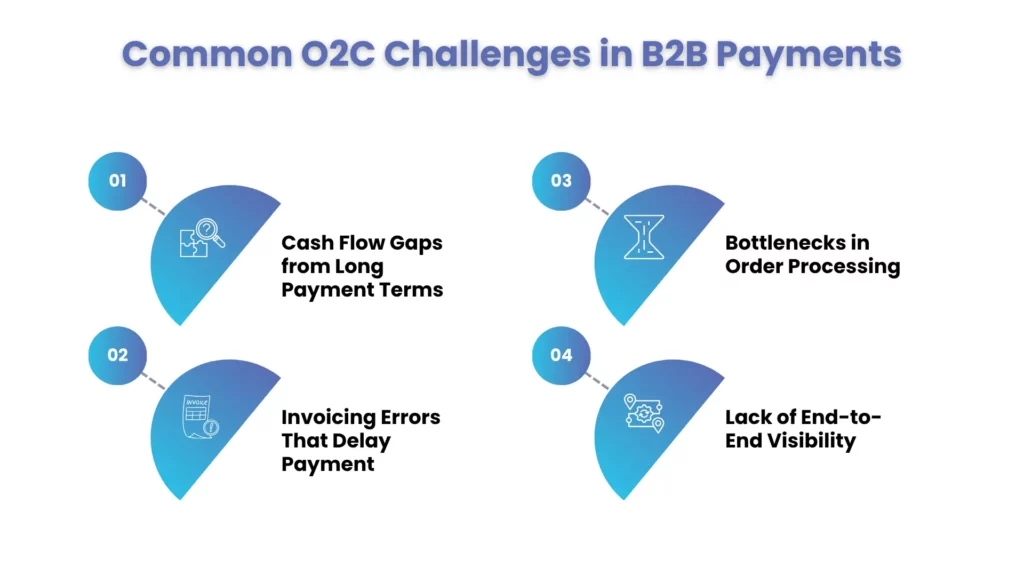

Common O2C Challenges in B2B Payments

Even well-run businesses run into friction in the O2C process. These are the issues that come up most often.

Cash Flow Gaps from Long Payment Terms

B2B payment terms can stretch 30 to 90 days. Nine out of ten businesses report being paid late for goods or services at some point. That combination — long terms plus late payment, puts sustained pressure on working capital. The antidote is clear terms, proactive reminders, and a collections process that kicks in before invoices become significantly overdue.

Invoicing Errors That Delay Payment

An incorrect invoice gives a customer a legitimate reason to withhold payment while the dispute is resolved. Common errors include wrong pricing, missing purchase order numbers, and incorrect billing addresses. A robust invoicing checklist, combined with automation where possible, catches most of these before they cause problems.

The SEC’s guidance on revenue recognition standards (ASC 606) is also relevant here, particularly for businesses with complex multi-element arrangements where invoicing timing directly impacts reported revenue.

Bottlenecks in Order Processing

If orders take too long to enter the system, or fulfillment is consistently delayed, it sets back the entire O2C process flow. Cross-functional visibility — with sales, operations, and finance working from a shared system, reduces these gaps significantly.

Lack of End-to-End Visibility

Without a unified view of where each order sits in the cycle, finance teams can’t tell which invoices need attention, which customers are at risk, or where the biggest delays are occurring. ERP systems, CRM integrations, and accounts receivable platforms help bring this visibility together, which is foundational to any end to end O2C transformation for B2B operations. See how finance and accounting services can provide this visibility as a managed function rather than a technology project.

How to Improve the Order to Cash Process

Knowing the steps and pain points is the starting point. Here’s what actually moves the needle when companies look at how to improve order to cash process performance.

- Set clear, documented payment terms upfront : Ambiguity in payment terms leads to disputes and delays. Every customer should know the due date, late payment consequences, and accepted payment methods before an order is placed. The Uniform Commercial Code (UCC) Article 2, maintained by Cornell’s Legal Information Institute and adopted across US states, governs many aspects of commercial payment terms, understanding it helps you draft terms that hold up.

- Automate wherever it reduces errors or speeds up steps: Invoice generation, payment reminders, and cash application are all strong candidates for order to cash automation. Tools range from ERP modules to standalone AR software, the goal is removing manual, repetitive steps that create lag and introduce errors.

- Monitor customer payment behavior: Tracking payment history by customer lets you anticipate risk, adjust credit limits proactively, and prioritize collections effort on accounts most likely to become problems.

- Build a real dispute resolution process: A clear path for customers to raise invoice disputes, with defined response times and owners, keeps relationships intact and prevents disputes from stalling the entire O2C process unnecessarily.

- Measure DSO and other cycle metrics consistently: What gets measured gets managed. If you don’t know your average Days Sales Outstanding, you can’t set a meaningful improvement target. Monthly or quarterly reviews of key order to cash process KPIs keep continuous improvement on the agenda.

People Also Ask:

What is the order to cash (O2C) process?

It’s the end-to-end workflow covering everything from a customer placing an order to your company collecting and applying payment, including credit checks, fulfillment, invoicing, and cash application.

What is the difference between O2C and OTC?

They’re the same thing. Order to Cash is sometimes abbreviated O2C and sometimes OTC.

What is DSO and why does it matter in O2C?

DSO (Days Sales Outstanding) measures the average time it takes to collect payment after a sale. Lower DSO means faster cash flow and a healthier O2C cycle.

What are the main steps in the order to cash cycle?

Credit management, order processing, fulfillment, invoicing, payment collection, cash application, accounts receivable management, and reporting.

How can businesses improve their O2C process?

By setting clear payment terms, automating invoicing and cash application, monitoring customer payment behavior, building a dispute resolution process, and tracking DSO consistently.

Ready to Fix Your Order to Cash Process?

If late payments, manual collections, or rising DSO are slowing your cash flow down, Corient can help. We streamline the full O2C cycle for US enterprises, so cash moves faster, with less effort from your team.

Conclusion

The order to cash cycle touches nearly every part of a B2B business, sales, operations, finance, and customer relationships. When the O2C process runs well, it’s almost invisible: orders flow in, invoices go out, and cash arrives predictably. When it doesn’t, the effects show up as cash flow gaps, strained customer relationships, and finance teams stuck in firefighting mode.

Whether you’re looking to reduce DSO, cut down on invoice disputes, or pursue a full end to end O2C transformation for B2B operations, the starting point is the same: understand each step of the cycle, measure where you’re losing time, and tackle the bottlenecks systematically.

The businesses that treat O2C as a strategic function, not just back-office admin, collect faster, manage risk better, and grow with fewer cash flow surprises. If you’d like expert support delivering a cleaner, faster O2C cycle, Corient’s Order to Cash services are built for exactly that.