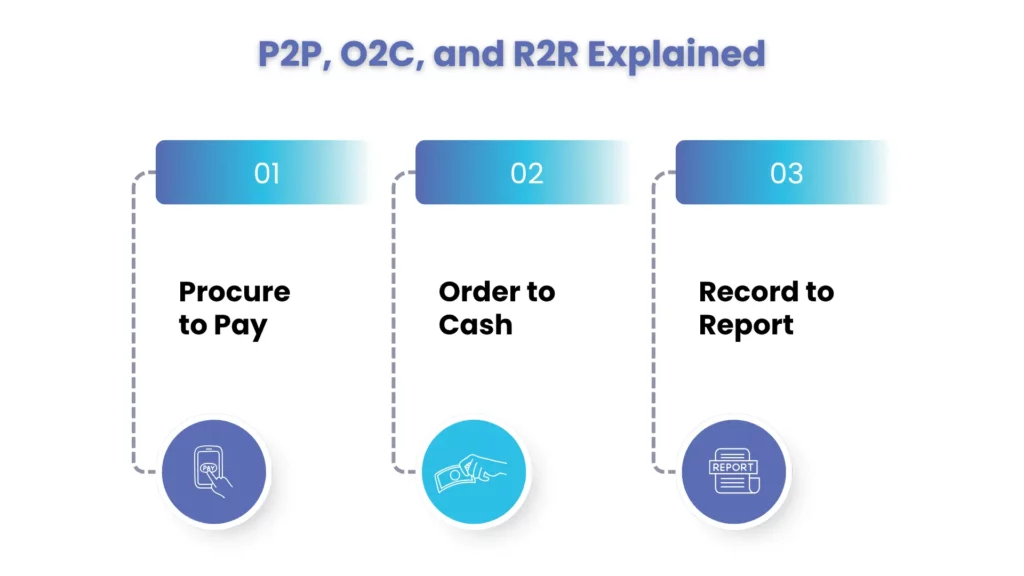

- P2P (Procure-to-Pay) is how your company buys things and pays vendors.

- R2R (Record-to-Report) is how those transactions get recorded and turned into financial statements.

- O2C (Order-to-Cash) is how you fulfill customer orders and collect payment.

Three different teams usually own these, procurement, accounting, and revenue operations, but every one of them is writing to the same general ledger. When the handoffs between Procure-to-Pay, Record-to-Report, and Order-to-Cash are clean, the month-end close is short and reporting is reliable. When they’re not, finance spends the first two weeks of every month untangling someone else’s data.

Here’s how the P2P process, R2R process, and O2C process each work, where U.S. companies most often lose time, and how the three fit together into one spend-to-cash loop.

Side-by-side comparison

| Process | Department | Purpose | Key Activities | Outcome When It Works |

| P2P (Procure-to-Pay) | Procurement & AP | Manage spend and vendor payments | Requisition → PO → Receipt → Invoice → Payment | Controlled spend, cleaner AP aging |

| R2R (Record-to-Report) | Accounting & FP&A | Record transactions and report financial results | Journal entries → Reconciliation → Close → Reporting | Faster close, audit-ready books |

| O2C (Order-to-Cash) | Sales & Finance | Convert customer orders into invoiced revenue and collected cash | Order → Credit check → Fulfillment → Invoice → Collection | Lower DSO, stronger cash flow |

The short version: The Procure-to-Pay (P2P) process manages outgoing payments, Record-to-Report (R2R) monitors how funds are used, and Order-to-Cash (O2C) ensures money flows back into the business. Together, they complete the entire spend-to-cash cycle.

Procure-to-Pay (P2P): the spend cycle

The Procure-to-Pay process turns “we need to buy something” into a paid vendor invoice. It runs through requisition, approval, purchase order, goods receipt, three-way match, and payment, typically via ACH, wire, or virtual card.

Done well, P2P is the single best lever a U.S. finance team has for cost control. Three things make the difference:

- Visibility — knowing what’s being committed before the invoice arrives, not after.

- Control — budgets, approval thresholds, and preferred-vendor logic applied at the point of purchase.

- Data quality — accurate GL coding, project tags, and cost center allocation that flow straight into reporting.

P2P also carries a few obligations that are easy to overlook until they bite. W-9 collection at vendor onboarding sounds basic, but missing W-9s are the most common reason 1099-NEC and 1099-MISC filings go sideways in January. Sales tax accrual on out-of-state purchases is another classic, use-tax exposure can sit dormant for years until a state audit surfaces it. A P2P process that captures vendor tax data, certificates of insurance, and W-9s before the first PO closes a lot of these gaps automatically.

For public companies and any private company on an IPO track, P2P is also where SOX controls live. Segregation of duties between requester, approver, and payer; documented approval thresholds; and an audit trail tying every payment back to a PO and a receipt, these aren’t nice-to-haves, they’re tested every year.

When P2P breaks down, invoices arrive without POs, AP chases approvals while early-payment discounts expire, and the accounting team inherits a pile of coding decisions at month-end. When P2P runs well, the data hitting R2R is already structured, and AP becomes a strategic function instead of a reactive one.

Order-to-Cash (O2C): the revenue engine

The Order-to-Cash process covers every step from the moment a customer places a confirmed order to the moment their payment clears the bank. O2C spans credit checks, order management, fulfillment, billing, collections, and revenue recognition under ASC 606.

O2C is where revenue quality is determined. Two specific things matter for U.S. companies:

ASC 606 compliance. Subscription and SaaS businesses live and die by performance obligations, transaction-price allocation, and recognition timing. If the contract terms feeding into the O2C process don’t match what’s getting recognized in R2R, your revenue numbers won’t survive an audit.

DSO and cash conversion. Net 30 is the assumption; reality is closer to net 45 in most B2B segments. A well-run Order-to-Cash cycle including smart use of O2C automation keeps orders, delivery confirmation, and invoices aligned so customers can’t park disputes against missing documentation.

When O2C data flows cleanly into Record-to-Report, finance has a reliable view of expected cash inflows, can model working capital with confidence, and gives the board a forecast that doesn’t need a caveat.

Record-to-Report (R2R): the financial control center

The R2R process takes everything happening in P2P and O2C and turns it into financial statements leadership and auditors can rely on. Record-to-Report covers journal entries, sub-ledger reconciliations, bank reconciliations, accruals, fixed asset accounting, intercompany eliminations, tax provision, and the actual close-and-report cycle.

R2R is where weak P2P and O2C surface as pain. A miscoded purchase shows up as a wrong expense line. A missing receipt creates a goods-received-not-invoiced (GRNI) balance that auditors flag. A customer payment that doesn’t match an invoice sits in a suspense account until someone reconciles it.

When the R2R process runs cleanly, companies close in five to eight business days, variances get explained early, and finance can spend the back half of the month on analysis instead of reconciliation. Under SOX 404 for public companies, this is also where control effectiveness is proven — and where deficiencies become disclosable.

Where the cycles actually connect

The handoffs between Procure-to-Pay, Order-to-Cash, and Record-to-Report are simple in theory and messy in practice. They aren’t, in practice.

A purchase approved in P2P becomes an AP entry R2R has to record correctly. A customer invoice generated in O2C affects revenue recognition, AR aging, and the cash flow statement all R2R territory. If a source transaction is wrong, R2R inherits the cleanup.

The breakdown is almost always at the transaction level. A PO is raised against the wrong cost center. A delivery happens in December but the invoice is dated January, so revenue lands in the wrong period. A vendor’s tax classification is captured incorrectly, so 1099 reporting goes wrong eleven months later. None of these are technology failures, they’re process gaps between cycles, patched manually during close, every single month.

The companies that pull ahead stop treating P2P, R2R, and O2C as separate departmental workflows and start treating them as one connected financial flow. P2P sets how money leaves, O2C defines how money comes in, and R2R proves both sides match. When the inputs are structured and consistent at source, finance spends less time fixing data and more time using it, for forecasting, scenario planning, and the kind of strategic input the CFO is actually being asked for.

For Example,

Imagine a large U.S. enterprise like a Fortune 500 consumer goods company with 25 manufacturing plants, 6,000 vendors, and customers across all 50 states plus 40 international markets. When the company issues purchase orders for $800 million worth of raw materials, packaging, ingredients, logistics services receives them at its facilities, runs three-way matching against POs and goods receipts, collects W-9s and certificates of insurance from new vendors, accrues use tax on out-of-state purchases, and pays 6,000 suppliers via ACH and virtual cards while capturing early-payment discounts, that’s P2P (Procure-to-Pay) running at scale. When the same company ships products to Walmart, Target, Costco, and thousands of smaller retailers, generates millions of invoices a month across subscription, milestone, and transactional billing models, manages customer credit limits, recognizes revenue under ASC 606 performance obligations, and collects $3 billion in monthly receivables, that’s O2C (Order-to-Cash) powering the revenue engine. At quarter-end, the corporate finance team consolidates ledgers from all 25 plants, automates intercompany eliminations, posts accruals, completes SOX 404 control testing, closes the books in 6 working days, and files the 10-Q with the SEC, that’s R2R (Record-to-Report) turning hundreds of millions of transactions into audited financial statements. Same three cycles as a corner coffee shop buy, sell, report only now they involve hundreds of millions of dollars, thousands of employees, Oracle Cloud ERP, a Global Business Services centre, and SEC-mandated disclosure timelines.

Stay ahead of your financial cycles

Get the latest best practices, expert insights, and compliance updates on P2P, R2R, and O2C, SOX-ready and built for US businesses, delivered straight to your inbox.

People Also Ask:

What is Procure to Pay (P2P)?

Procure-to-Pay (P2P) is the end-to-end process of acquiring goods and services and paying suppliers. It covers everything from requisitions and purchase orders to receiving, invoice reconciliation, and payment. P2P is essential for streamlining procurement operations and optimizing business spend.

What is Order to Cash (O2C)?

Order-to-Cash is the mirror image of P2P but on the revenue side. It covers everything from receiving a customer order to generating a compliant invoice and collecting payment. For US businesses, this includes credit checks, revenue recognition under ASC 606, and collections management. A smooth O2C process shortens your DSO, strengthens cash flow, and keeps your revenue numbers audit-ready.

How does Record to Report (R2R) differ from P2P?

P2P controls how your company spends and pays vendors. R2R takes those transactions and turns them into accurate financial statements, reconciliations, and compliance reports. Simply put: P2P executes the spend, R2R records and reports it.

Do we need a separate system for each cycle?

Not necessarily. Many mid-market companies run all three from a connected ERP like NetSuite, Sage Intacct, or Microsoft Dynamics, with specialized tools layered on for procurement, order management, or AP automation. What matters is that data flows cleanly between cycles, not how many logos are in the stack.

How does SOX fit into this?

SOX controls touch all three cycles. P2P controls cover purchase approvals and payments. R2R controls cover the close and reporting process. The O2C process covers revenue recognition under ASC 606. For public companies and pre-IPO companies, these are tested every year.

Where should we start if all three feel broken?

Start with the Procure-to-Pay process. It produces the cleanest wins fastest, vendor onboarding, approval workflows, and spend visibility, and the data improvements show up in Record-to-Report within one or two close cycles.

Conclusion:

P2P, R2R, and O2C aren’t three competing processes. They’re three lenses on the same financial reality. Run Procure-to-Pay, Order-to-Cash, and Record-to-Report as a connected system with shared data, clean handoffs, and consistent coding at the source — and your finance team stops auditing history and starts shaping what comes next.

Whether you’re a growing startup or an established enterprise, getting these three cycles to work as one is what separates a reactive finance team from a strategic one. At Corient, we help US businesses build that connected system SOX-compliant, US GAAP-ready, and built to close faster, report with confidence, and give your CFO the numbers that actually drive decisions.