Days Sales Outstanding (DSO) is a financial metric that measures the average number of days it takes a company to collect payment after making a credit sale. It’s calculated by dividing average accounts receivable by net revenue, then multiplying by the number of days in the period. A lower DSO indicates faster cash collection and stronger liquidity.

Understanding how to calculate DSO is one of the fastest ways to spot whether your collections process is working the way it should, and once you know the formula, tracking it consistently can reveal cash flow issues before they become a real problem.

What Is Days Sales Outstanding?

Days Sales Outstanding (DSO) is a working capital metric that shows how efficiently a company converts credit sales into actual cash, a core input into broader cash flow management. In simple terms, it tells you the average number of days your business waits between making a sale on credit and receiving payment for it. Once you know how to calculate DSO, it becomes one of the fastest ways to spot whether your collections process is working the way it should.

Key takeaways:

- Days Sales Outstanding measures the average time a business takes to collect payment after a credit sale is made.

- A lower Days Sales Outstanding points to faster collections and stronger cash flow; a higher Days Sales Outstanding signals collection delays and added risk.

- Benchmarks differ by industry, many businesses target 30 to 60 days, though sectors with longer project cycles often run higher.

- Tracking Days Sales Outstanding consistently helps finance and sales teams plan cash flow, sharpen collections, and manage revenue more effectively.

- Knowing the DSO calculation formula (and the AR days outstanding formula behind it) lets any finance team calculate DSO accurately, without relying on guesswork.

How to Calculate Days Sales Outstanding (DSO)

If you’re wondering how to calculate days of sales outstanding, the short answer is: DSO calculation is typically done on an annual basis for consistency, using the average accounts receivable balance rather than a single point-in-time figure. This avoids a mismatch between when receivables are measured and when revenue is recognized.

Accounts receivable (A/R) sits on the balance sheet and represents the value of goods or services already delivered to customers, recognized as revenue under accrual accounting, for which cash hasn’t been collected yet.

Since customers can typically choose to pay in cash or on credit, credit purchases give them more time after the sale to fulfill their payment obligation. Because Days Sales Outstanding reflects how long that collection takes, a lower number is always preferable to a higher one.

- Lower DSO → The company converts credit sales into cash quickly, and receivables sit on the books for a shorter time before being collected.

- Higher DSO → The company takes longer to convert credit sales into cash, and receivables remain outstanding longer, reducing available liquidity.

DSO Calculation Formula (AR Days Outstanding Formula)

To calculate DSO, divide the accounts receivable balance by revenue for the period, then multiply by the number of days in that period (typically 365 for an annual view). This is also commonly referred to as the AR days outstanding formula, since it measures how many days’ worth of sales are sitting in accounts receivable at any given time.

Where:

- Average Accounts Receivable = (Ending A/R + Beginning A/R) ÷ 2

- Net Revenue = Gross Revenue − Returns − Discounts

This is the core DSO calculation formula most finance teams rely on, and it’s the same formula whether you’re calculating DSO monthly, quarterly, or annually; only the “number of days” in the multiplier changes (30, 90, or 365 respectively).

Days Sales Outstanding matters because faster cash collection directly improves liquidity, the amount of cash a business actually has on hand to work with.

- Liquidity Risk → More cash on hand reduces the risk of shortfalls when obligations come due, the value here is fairly intuitive.

- Cash Flow Generation → Cash collected sooner (rather than sitting in receivables) can be redeployed into reinvestment or capital expenditure where it can generate a return, instead of sitting idle waiting to be collected.

DSO Calculation Example: How to Calculate DSO Step by Step

DSO = (Accounts Receivable ÷ Total Credit Sales) × Number of Days in Period

Say a company has an accounts receivable balance of $45,000 and generated $270,000 in revenue over the period. Here’s how to calculate DSO for this scenario:

- Dividing $45,000 by $270,000 gives 0.1667, or 16.7%

- Multiplying 16.7% by 365 days gives a DSO of approximately 61 days

This means that once a sale is made, the company typically takes about 61 days to actually collect the cash for it. Running this same DSO calculation every month or quarter, with updated A/R and revenue figures, is what lets a business track whether collections are speeding up or slowing down over time.

| Metric | Value |

| Accounts Receivable (A/R) | $45,000 |

| Revenue | $270,000 |

| A/R as % of Revenue | 16.7% |

| Days Sales Outstanding (DSO) | ≈ 61 days |

At this point, the product or service has already been delivered and the revenue recognized under accrual accounting, but the cash itself hasn’t landed yet. All that’s left is for the customer to complete the payment.

As with days inventory outstanding (DIO), some companies use the average A/R balance (beginning plus ending, divided by two) to better align the timing of the numerator and denominator. In practice, though, many businesses simply use the ending balance for simplicity, since the difference rarely has a material effect on forecasts.

What Is a Good Days Sales Outstanding (DSO)?

If a company’s Days Sales Outstanding is trending upward compared to prior periods, that’s usually a red flag, it means more time is needed to collect cash from credit sales, pointing to operational inefficiencies worth investigating.

If Days Sales Outstanding is trending downward, that’s a good sign: the company is getting more efficient at turning sales into cash.

As a general principle, businesses aim to keep Days Sales Outstanding as low as possible, since a lower number reflects a more efficient collections process.

Remember: an increase in a working capital asset (like A/R) reduces free cash flow, while an increase in a working capital liability increases it. So a rising A/R balance represents cash going out the door (in effect), while a falling A/R balance means the company has been paid and now holds more liquidity.

- Decreasing DSO → Efficient cash collection → Higher free cash flow

- Increasing DSO → Inefficient cash collection → Lower free cash flow

There’s an exception for seasonal or cyclical businesses, where sales concentrate heavily in certain quarters or swing with broader economic conditions, DSO can look distorted in isolated periods for reasons that have nothing to do with collections efficiency.

It’s also worth noting that comparing only credit sales (rather than total net sales) is technically the more accurate approach, but most public companies don’t break out cash vs. credit sales in their financial filings, so real-world DSO calculations often use total revenue as a practical stand-in.

Context matters more than the raw number.

A DSO of 90 days might be entirely normal for a heavy-equipment manufacturer selling to enterprise clients on long payment cycles. That same 90-day DSO would be a serious warning sign for a fast-moving retail apparel business, where the collection cycle should typically run in weeks, not months. For our hypothetical retailer, a DSO that far above the norm would suggest it’s time to revisit collection practices, especially if it’s trailing industry peers.

How to Lower Days Sales Outstanding (DSO)

For companies whose Days Sales Outstanding runs meaningfully higher than industry peers, common corrective steps include:

- Limit or discourage credit payments : or offer discounts as an incentive for customers who pay in cash upfront.

- Flag repeat late payers : apply targeted restrictions, such as requiring upfront payment for customers with a pattern of delays.

- Run credit background checks : particularly important for customers on installment-based payment agreements.

That said, a longer DSO isn’t always a sign of poor management. Sometimes it reflects the negotiating leverage of a major customer who represents a significant share of revenue and has pushed for extended payment terms. In these cases, it’s important to weigh not just industry norms and the nature of the product or service sold, but the specific dynamics of the customer relationship. A large, long-standing customer with a clean payment history isn’t necessarily a red flag, even if their payment cycle runs longer than average.

Common Use Cases for Tracking DSO

Companies track Days Sales Outstanding not just as a reporting metric, but as an active input into financial decision-making. Common applications include:

Cash flow planning:

A stable DSO helps finance teams predict when revenue will actually convert into usable cash. If DSO runs around 50 days, leadership knows that cash from a January sale likely won’t land until late February, which shapes decisions around vendor payments and payroll timing.

Credit and collections management:

Tracking DSO at the account level surfaces early warning signs. If a specific client’s average payment cycle stretches from 25 days to 55 days, finance can step in early, reviewing terms, escalating reminders, or looping in the sales team to resolve the underlying issue.

Benchmarking against peers:

Comparing DSO to industry averages reveals whether collections are actually efficient or just look fine in isolation. A software company running a DSO of 65 days against a peer average of 40 days has a clear signal to dig into invoicing accuracy, approval workflows, or credit policies.

Sales and revenue forecasting:

Sales leaders use DSO trends to understand the real timing of cash inflows, which can shape how deals are structured, for instance, negotiating upfront deposits or milestone-based payments on larger contracts.

Investor and stakeholder reporting:

A DSO that’s consistently low, or steadily improving, is a straightforward way to demonstrate liquidity discipline and operational health in financial reporting.

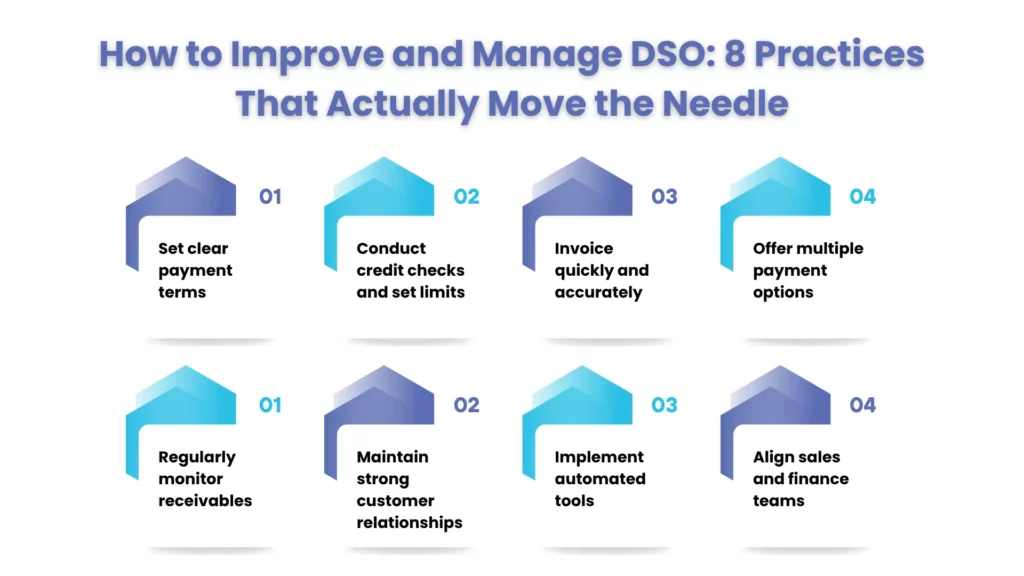

Tips and Best Practices for Improving and Managing DSO

Strong Days Sales Outstanding management, a core piece of revenue lifecycle management, translates into more available cash, better customer relationships, and more room to invest in growth. These best practices help businesses get paid faster while keeping customer relationships intact.

- Set clear payment terms

Payment expectations should be communicated early and reinforced consistently. Display terms clearly on every invoice and contract, and consider early-payment incentives to encourage faster turnaround. Revisit these terms periodically to make sure they still align with business goals and current industry norms. - Conduct credit checks and set limits

Before extending credit, evaluate each customer’s financial reliability and start conservatively. Credit limits can be increased over time as trust is established. A consistent, regularly updated policy helps balance growth with protection against late payments. - Invoice quickly and accurately

Send invoices immediately after a sale closes or a milestone is completed. Use a standard checklist to make sure every invoice includes the necessary details, which reduces disputes and delays. Automated invoicing tools can generate and send invoices the moment a sale is finalized, cutting down both processing time and human error, and should ideally support multiple billing frequencies (monthly, quarterly, annual). - Offer multiple payment options

Give customers several ways to pay, online payments, automatic bank transfers, or a self-service customer portal that consolidates invoices across sales channels. The easier it is to pay, the sooner customers tend to do it. - Regularly monitor receivables

Review accounts receivable on a weekly basis to catch payment issues early. Set up automated reminders for both upcoming and overdue invoices, and use a tiered escalation process, starting with friendly nudges and moving to more formal follow-ups for accounts that stay overdue. Assign clear ownership of this process to one team member for consistency. - Maintain strong customer relationships

Keep communication open. If a payment is late, reach out to understand why and work toward a solution together, a short-term payment plan, for example. Regular check-ins can help surface payment issues before they become a pattern, and a simple feedback loop can help refine billing and payment processes over time. - Implement automated tools

Accounting and AR automation software can streamline invoicing, reminders, and aging reports, while reducing manual errors. Look for a system that integrates with your existing tech stack, provides real-time visibility into DSO performance, and can handle more complex billing scenarios. Predictive analytics and AI-driven sales tools can also help flag likely payment delays before they happen. - Align sales and finance teams

Make sure sales understands why Days Sales Outstanding matters, they play a direct role in setting customer expectations around payment terms during the sales process. Consider incorporating Days Sales Outstanding performance into sales metrics, which encourages reps to prioritize deals with customers who have strong payment histories. Regular syncs between sales and finance help catch DSO issues before they compound.

Bring Your DSO Down with Corient

Managing DSO manually can pull focus from higher-value finance work. Corient’s O2C Process help you streamline invoicing, tighten credit policies, and speed up collections, so cash keeps moving in.

People Also Ask:

What is a good DSO benchmark for Business?

Below 30 days is best-in-class. 35–45 days is the industry average according to the Credit Research Foundation. Above 60 days needs immediate process review. SaaS and professional services companies typically achieve sub-30-day DSO; manufacturing and distribution often run 50+ days due to longer payment terms.

How fast does automation deliver DSO results?

Expect a 3–7-day improvement within the first 60–90 days. As credit policies and e-invoicing scale across the client portfolio, organizations typically see a 15–25-day reduction after 6–12 months.

What is the difference between DSO and Best Possible DSO (BPDSO)?

BPDSO assumes every client pays exactly on their agreed terms. The gap between your actual DSO and BPDSO reveals how much of your problem is internal process inefficiency versus genuine client behavior.

Will these strategies hurt client relationships?

No. E-invoicing, self-service payment portals, and dynamic discounting improve the buyer experience by reducing friction. Smart escalation protocols protect strong relationships while addressing late payers through structured, non-confrontational workflows.

How does DSO impact credit rating?

High DSO signals cash flow weakness to lenders, which leads to higher borrowing rates and tighter covenants. A declining DSO demonstrates financial discipline and can unlock better financing terms.

What are the fastest ways to start reducing DSO?

Some of the most effective first steps include setting clear payment terms on every invoice, invoicing quickly and accurately, offering multiple easy payment options, and reviewing receivables weekly with automated reminders. Aligning sales and finance teams so reps understand the impact of payment terms also helps prevent DSO issues before they start.

Conclusion:

Days Sales Outstanding is more than an accounting formula, it’s a direct reflection of how well a business turns sales into usable cash. A rising DSO quietly drains liquidity and limits how much a company can reinvest in growth, while a well-managed DSO frees up cash, strengthens forecasting, and signals financial discipline to investors and stakeholders alike.

There’s no universal “good” number, what counts as healthy depends heavily on your industry, deal size, and customer mix. What matters more is the trend: a DSO that’s holding steady or improving over time usually means collections, credit policy, and invoicing are working the way they should. A DSO that’s creeping upward is worth investigating before it becomes a cash flow problem.

The good news is that DSO is highly manageable. Clear payment terms, disciplined credit checks, fast and accurate invoicing, consistent receivables monitoring, and close alignment between sales and finance can meaningfully bring DSO down, often without changing pricing or losing customers in the process. Treat DSO as a metric to track continuously, not a number to check once a quarter, and it becomes one of the most reliable early-warning systems a finance team has.

Struggling to bring DSO down? Corient’s Order to Cash Services team can help streamline invoicing, credit, and collections end-to-end. Get in Touch Today.