When a large business fails SOX compliance, it faces SEC investigations typically initiated within 30–90 days, mandatory restatement of financial statements, executive fines up to $5 million, imprisonment of up to 20 years for willful violations, and potential delisting from NYSE or NASDAQ. The financial, legal, and reputational damage consistently exceeds the cost of maintaining compliance.

Besides, non-compliance leads to a loss of investor trust, higher interest costs, and millions of dollars’ worth of corrective measures costing an average of $2.8 million per organization over 18-24 months. The risks are higher than ever given the SEC’s new enforcement team that is focused on auditor failures, which will have the 2026 tag on their work.

Purpose and Benefits of SOX Compliance

SOX was designed to restore investor trust in financial reporting by:

- Ensuring investors are not misled by inaccurate financial information

- Establishing internal control measures to prevent financial misstatements

- Holding CEOs and CFOs personally and criminally accountable for financial reporting accuracy

- Strengthening the independence of external audits through PCAOB oversight

Beyond SOX regulatory compliance, companies with robust SOX programs typically demonstrate stronger operational efficiency, lower fraud risk, reduced audit fees over time, and higher investor confidence — all measurable business advantages.

Key Requirements for SOX Compliance

| SOX Section | Title | Core Requirement | Penalty for Violation |

| 302 | Corporate Responsibility | CEOs/CFOs must personally certify accuracy of financial reports | Fines + criminal liability Fines up to $5M + up to 20 years imprisonment |

| 404 | Internal Controls Assessment | Annual ICFR report, attested by external auditors for large accelerated filers | Material weakness disclosure; restatement risk |

| 301 | Audit Committee | Committee must be Fully independent; handle whistleblower complaints | SEC enforcement action |

| 409 | Real-Time Disclosure | Material changes (financial condition, operations)must be disclosed quickly | SEC investigation |

| 802 | Record Retention | Retain financial records and audit workpapers for 7 years | Up to 20 years imprisonment for willful destruction |

| 906 | Criminal Penalties | Certifying false reports is a federal crime | Fines up to $5M + imprisonment |

What Happens When a Large Business Fails SOX Compliance?

A common failure point for large organizations is the record-to-report process. Issues here can trigger a chain reaction of compliance problems, making it easier for a business to fail SOX requirements.

SEC Scrutiny and Investigations

The SEC’s newly established SOX Group (March 2026) specifically targets audit firm misconduct and ICFR deficiencies with a mandate for faster enforcement action. The public disclosure of an SEC investigation typically causes immediate and significant damage to stock price and investor confidence — though the precise magnitude varies widely by company and circumstances.

Mandatory Restatement of Financial Statements

Organizations may be required to restate previously filed financial statements — a public admission that prior reporting was inaccurate. Restatements frequently trigger shareholder class-action lawsuits, credit rating reviews, and immediate institutional selling. According to the GAO’s June 2025 report on SOX compliance, companies that announced restatements were more likely to have had weak internal control over financial reporting.

Delisting Risk

If there is continued failure to comply, or to file reports on time, the company may be delisted from the major exchanges (NYSE or NASDAQ).

Loss of Investor and Lender Confidence

Positions can be divested by institutional investors. Lenders can increase interest rates or may require a credit line to be called for due to a liquidity crisis.

Operational Disruption

Internal remediation, audit re-engagement, and compliance overhauls consume enormous management bandwidth. According to KPMG’s 2025 SOX Survey, the average SOX program costs $2.3 million and 15,581 person-hours annually, and remediation programs following a failure run significantly higher.

Penalties for Non-Compliance With SOX

SOX carries some of the harshest penalties in U.S. corporate law, split across civil and criminal categories.

Civil Penalties

- SEC cease-and-desist orders

- Clawbacks of executive bonuses and profits tied to misreported financials

- Bars on serving as an officer or director of a public company

- Court-ordered remediation mandates

Criminal Penalties

- Fines up to $5 million for executives who knowingly certify false financial reports

- Up to 20 years imprisonment under Sections 302 and 906

- Enhanced penalties under Section 802 for willful destruction or falsification of audit records

The SEC has announced enhanced enforcement priorities, with increased scrutiny of audit firm quality controls and ICFR deficiencies going forward.

The Most Common Reasons Large Businesses Fail SOX Compliance

Around 20-25% of all public companies in the United States have at least one material weakness every year. The first step in creating a more robust SOX compliance checklist is to know what causes large businesses to fail and the most common ones are:

Inadequate Internal Controls

Untested controls or financial reporting that is not well documented or tested may result in external auditors finding that there are material weaknesses. If auditors can’t verify a control operates effectively, it doesn’t count — regardless of intent.

Insufficient Segregation of Duties

The ability of the same person to initiate and approve transactions raises the risk for fraud and is a direct violation of SOX.

IT General Control (ITGC) Failures

Some of the most common issues found in an audit include access management, change management, and system operations controls. This is where it can adversely affect the trustworthiness of the automatic financial controls.

Lack of Audit Readiness

Many large organizations conduct audits as an annual event, not an ongoing process and this can result in gaps at audit time.

Rapid Organizational Change

Existing SOX frameworks typically do not address control gaps that are often created during mergers, acquisitions, restructurings and system migrations.

Poor Documentation

If it’s not documented, it didn’t happen, for SOX audits. So, for SOX audits if the controls were not documented they were not controls in practice.

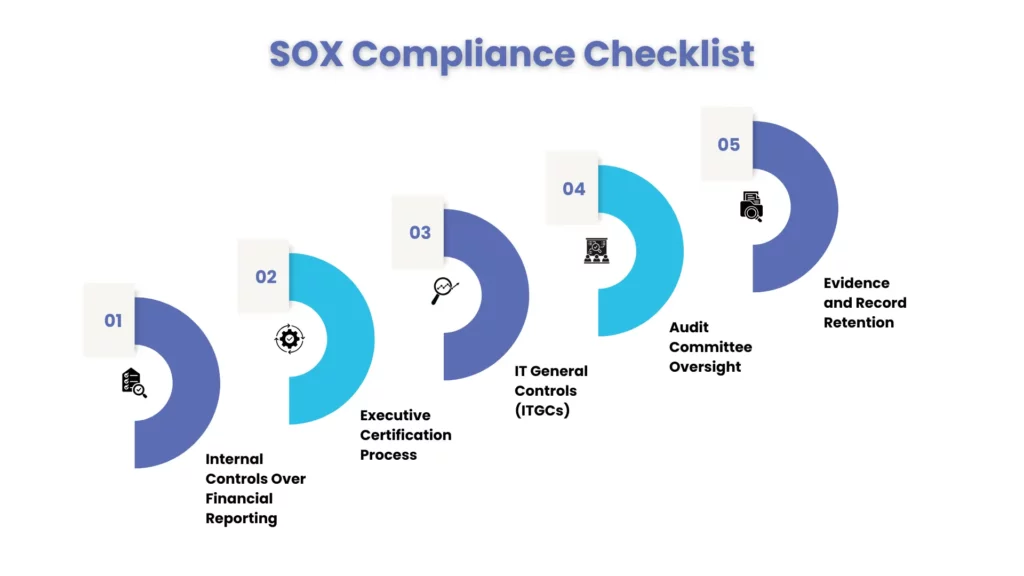

SOX Compliance Checklist – What Large Businesses Must Have in Place

Meeting SOX compliance checklist requirements demands a comprehensive, year-round program. The following five pillars form the core of any effective sox compliance requirements framework for large businesses:

1.Documented Internal Controls Over Financial Reporting (ICFR)

Every key control must be mapped to financial reporting risks, clearly documented, and regularly tested. Controls should align with the COSO 2013 framework, which remains the de facto standard for Section 404 attestations.

2. Executive Certification Process

Establish a formal process for CEO and CFO review and sign-off on internal control assessments prior to financial statement filings. This process should include sub-certification from business unit leaders.

3. IT General Controls (ITGCs)

Maintain robust controls over user access management, change management, and computer operations. Given the increasing reliance on automated financial systems, ITGC failures can compromise the entire control environment.

4. Audit Committee Oversight

Ensure the audit committee maintains independence, meets regularly, and has clear procedures for receiving and addressing whistleblower complaints in accordance with Section 301. and have direct lines of communication with the external auditor — separate from management.

5. Evidence and Record Retention

Maintain audit trails and retain all relevant financial record to report process, work papers, and electronic communications for a minimum of seven years as required under Section 802.

Preparing for a SOX Audit – What Large Businesses Need to Do

It takes time to prepare for a SOX audit, and it’s not something that can be done at the last minute. Preparing for an audit is an on-going process, and a discipline that large businesses that consistently achieve success treat as such, beginning with an annual risk assessment to determine and prioritize financial reporting risks. It is important that these risks are mapped to controls, tested throughout the year and any control deficiencies, whether minor, significant or material, are acted upon immediately and escalated if necessary.

Early coordination with external auditors assists in setting a scope, timing and evidence for the audit. The centralized controls repository helps to clearly track ownership, test results, and remediation status; and regular training and updated documentation hold control owners accountable and keeps processes up to date.

SOX Compliance Solutions – How Large Businesses Can Get Back on Track

The SEC comment letter or adverse audit opinion from a large business is a serious issue and immediate action is key. Use a root cause analysis to determine the root cause, and develop a remediation plan that includes clear owners, timelines and milestones. Permanent controls can be implemented but interim controls can help reduce risk while permanent controls are put in place.

This helps to speed up remediation and provides independent validation. Incorporating technology solutions such as GRC platforms and automated controls monitoring streamlines testing, enhances evidence collection, and offers real-time visibility ensuring organizations can efficiently restore SOX compliance and remain audit ready.

SOX Compliance in 2026 – What’s Changed

The financial reporting environment is continuously changing, as is the SOX regulatory compliance environment. Here are five important developments to keep an eye on that will impact large business in 2026:

SEC SOX Enforcement Group (March 2026)

New group to monitor audit firm misconduct, tougher audit firm controls and failure of ICFR, and more expediated enforcement action.

Updated PCAOB Standards (AS 1000 & AS 1105)

More stringent evidence thresholds; omissions could be where companies have performed well in the lighter touch audits before.

ESG & Sustainability Reporting Controls

Sustainability expands to controls in COSO ICSR supplement and ESG integration is necessary for SEC climate disclosure requirements.

Increased Focus on IT Controls

Increased focus on ITGCs, particularly access and change management, due to growing automation & cloud-based financial systems.

Common SOX Compliance Mistakes to Avoid

Management’s word without approvals, records, or results all controls have to be backed up with approval, record, or test results.

- Failure to establish IT control risk: ITGC failures can have a domino effect in the automated financial reporting process.

- Failure to monitor remediation: unresolved deficiencies that are present on future audits are creating an increasing enforcement risk.

- Not scoping AI and automation into ITGC: Finance teams using AI tools for material processes without corresponding controls are carrying undisclosed SOX risk.

- Ignoring cybersecurity’s financial reporting dimension: A cyber incident that affects the integrity or timeliness of financial data is a SOX event. Organizations without a documented cyber-materiality assessment process are non-compliant.

Failing to re-evaluate controls following an organizational change (such as restructuring, migrations, or mergers) a SOX impact assessment is always needed following an organizational change.

How Corient Can Help with SOX Compliance

SOX compliance is one of the most challenging regulatory requirements for large companies and the potential consequences go well beyond finance. Corient has a knowledgeable team that assists organizations meet compliance, efficiency and audit requirements. Corient’s advisory team brings specialized experience across SOX program design, ITGC, and audit readiness for large, complex organizations.

- Internal Controls & Compliance with SOX requirements

- Readiness assessment & gap analysis

- Determine, document and test internal controls

- ITGC review & remediation support

- Reporting on the audits and certification by the executive.

- Managed SOX Compliance Services are provided to address ongoing compliance needs.

With Corient you get a SOX program that is compliant, sustainable and in line with your internal teams and external auditors.

People Also Ask:

What is SOX compliance and who does it apply to?

Compliance to SOX involves making sure that the accounting processes are done right and that appropriate internal control measures are established. Compliance with SOX applies to all public companies operating in the United States, subsidiaries of such companies, and even to foreign companies operating within the U.S.

What are the penalties for non-compliance with SOX?

:The sanctions against non-compliance with the SOX Act are severe, including fines and criminal charges, SEC investigation, re-statement of financial record to report process, delisting from exchanges, and suits by shareholders. Those who submit erroneous reports may be fined a maximum of $5 million and spend up to 20 years in jail.

How should a large business start preparing for a SOX audit?

To prepare for a SOX audit, start by identifying financial reporting risks and making sure your controls are mapped, tested, and well-documented. Assign clear owners and keep evidence ready. Treat audit prep as an ongoing process, not a last-minute scramble.

What is the difference between SOX compliance and SOC compliance?

SOX compliance is a U.S. law requiring public companies to maintain accurate financial reporting and strong internal controls, with serious penalties for violations. SOC reports, like SOC 1 or SOC 2, are voluntary audits that show clients a company’s controls are effective. In short, SOX is mandatory and legal, while SOC is optional and for trust-building.

How has SOX regulatory compliance changed in 2026?

In 2026, the SEC created a new SOX enforcement group to crack down on audit firm issues and control failures, increasing regulatory scrutiny. Auditing standards have also been tightened, and with the COSO framework now covering sustainability reporting, companies should start including ESG controls in their SOX programs.

Conclusion

For large businesses, SOX compliance is not a checkbox exercise it is a core responsibility that supports investor trust, market access, and executive accountability. Failing to meet requirements can trigger consequences far more costly than maintaining compliance from the start.

At Corient Business Solutions, we provide structured guidance and support to help organizations maintain a strong SOX program. With the right framework, team, and year-round approach to control testing and documentation, compliance is achievable even in complex, high-growth enterprises.