A trial balance in accounting is a statement that lists all ledger accounts and their closing debit or credit balances on a specific date, used to verify that total debits equal total credits before preparing financial statements. It is a core step in the double-entry bookkeeping cycle and is mandatory for Indian businesses filing GST returns, complying with the Companies Act 2013, or preparing for a CA audit — all of which depend on accurate finance and accounting services.

Most of the accounting mistakes do not declare themselves. Transposed figures, missing credits or journal entries posted in the wrong account can subtly skew your books as a whole. Early identification of such mismatches becomes a must for Indian firms that have to file GSTR-9 annual returns, maintain books under the Companies Act 2013, or present audited financials to lenders and the Ministry of Corporate Affairs (MCA).

This guide covers the trial balance in accounting format, the three types of trial balance, a step-by-step preparation process, a worked Indian example using ₹ figures for the financial year 2024–25 (April–March), how to prepare a trial balance in Tally ERP / Tally Prime, common errors, and the limitations you must keep in mind for accurate financial reporting.

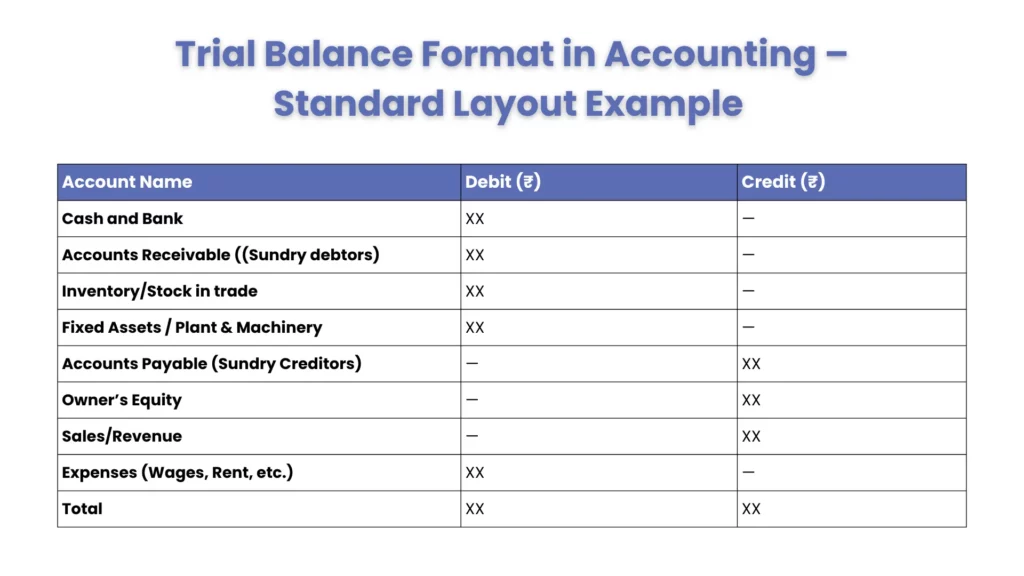

Trial Balance Format in Accounting – Standard Layout with Indian Example

A standard trial balance is a worksheet with three columns, designed for clarity before preparing the income statement (Trading & Profit/Loss Account) and Balance Sheet under Schedule III of the Companies Act 2013. It forms the critical final checkpoint in the Record to Report (R2R) process.

Standard Layout Example:

Key Formatting Rules:

- Account Name Column: Displays all the ledger accounts in the order that they appear in the chart of accounts (the order is Assets, Liabilities, Equity, Income, Expenses).

- Debit Column: This column will show the ending debit balance of each account.

- Credit Column: Closing credit balance of each account.

- Totals must match: if they do not, they are a ledger error.

- Indian businesses typically add a fourth column for the Ledger Folio (L.F.) number, which cross-references each balance to its source page in the ledger book — a practice recommended under ICAI bookkeeping guidelines.

Types of Trial Balance in Accounting – Which One Are You Preparing?

Unadjusted Trial Balance:

Prepared immediately after posting all regular journal entries to the general ledger, before any period-end adjustments are made. Trial balance in accounting reflects raw ledger balances and is used as the starting point for identifying what still needs correction.

Adjusted Trial Balance:

Prepared after recording accruals, prepayments, depreciation (as per the Companies Act 2013 Schedule II), and deferred income entries. Trial balance in accounting carries accurate, period-end figures and serves as the direct basis for drafting financial statements.

Post-Closing Trial Balance:

Prepared after all nominal accounts (income and expense accounts) have been closed to the Profit & Loss Account or retained earnings. Trial balance in accounting includes only permanent balance sheet accounts, confirming books are clean for the next accounting period.

| Type | When prepared | What it Includes | Used to Prepare |

| Unadjusted | After Journal entries are posted | All ledger balances before adjustments | Identify adjustments needed |

| Adjusted | After adjusting entries are recorded | Updated balances including accruals and deferrals | Income statement & balance sheet |

| Post-Closing | After closing entries are made | Permanent accounts only (assets, liabilities, equity) | Opening balances for the next period |

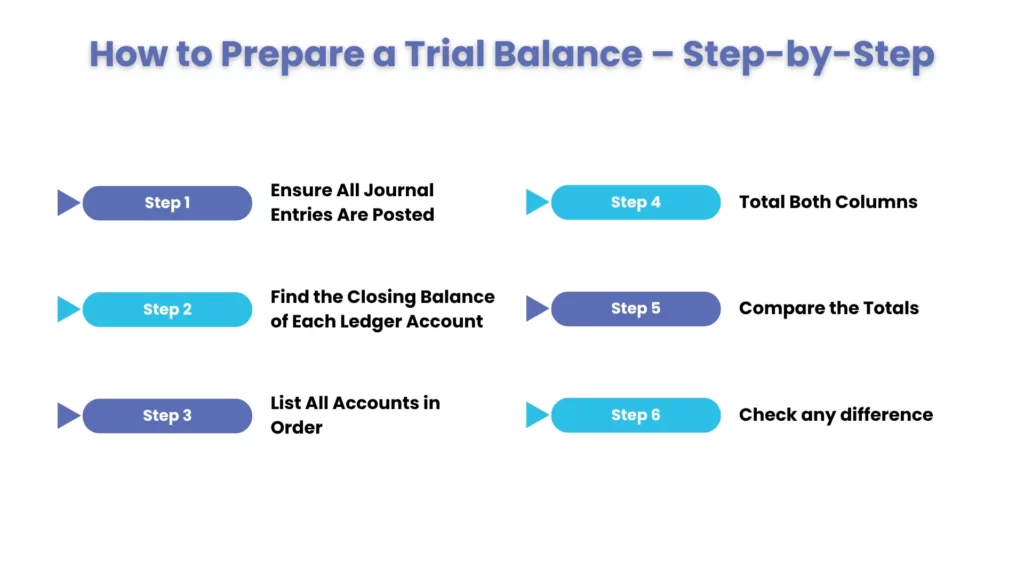

How to Prepare a Trial Balance – Step-by-Step

To grasp the concept of trial balance in accounting, one must have an idea of the mechanics of a ledger and the logical order of events that leads to the trial balance. Let’s get a step-by-step breakdown below.

Step 1: Ensure All Journal Entries Are Posted

Make sure that all journal entries have been made prior to creating a trial balance in accounting, and that all journal entries have been posted to the appropriate general ledger accounts. Incomplete Balances will be awarded for any unposted entries.

Step 2: Find the Closing Balance of Each Ledger Account

For each account in your general ledger, add up all of the debit items and credit items on the account, and find the closing balance of the account. A Debit balance means that there are more debits than credits in an account and a credit balance means that there are more credits than debits in an account.

Step 3: List All Accounts in Order

Accounts listed in normal chart of accounts format assets first followed by liabilities, equity, income and expenses. Record the closing balance of each account, putting the numbers in the Debit or Credit column.

Step 4: Total Both Columns

Add up all figures in the debit column and separately add up all figures in the credit column. Write both totals on the bottom of the worksheet.

Step 5: Compare the Totals

If the totals of the debits and credits are equal, then the trial balance is in balance and you can now prepare your financial statements. If they don’t correspond, there is an error in the ledger which needs to be detected and rectified before proceeding.

Step 6: Check any difference

If the totals differ, re-trace journal entries and ledger postings. If the difference is divisible by 9, suspect a transposition error. If it matches a specific transaction, that entry likely has a missing side. Open a Suspense Account as a temporary measure to hold unresolved differences while investigation continues.

Tally Tip: In Tally Prime or Tally ERP 9, the Trial Balance report is accessible under Gateway of Tally → Display More Reports → Trial Balance. You can drill down into any account to view individual vouchers, making error-tracing significantly faster than manual methods.

Trial Balance Example in Accounting – A Worked Illustration

Below is a trial balance v for ABC Traders, a sole proprietorship based in Mumbai, as of 31 March 2025 — the end of the Indian financial year.

| Account Name | Debit (₹) | Credit (₹) |

| Cash and Bank | 85,000 | — |

| Accounts Receivable (Sundry Debtors) | 42,000 | — |

| Inventory / Closing Stock | 63,000 | — |

| Office Equipment | 1,20,000 | — |

| Accumulated Depreciation | — | 24,000 |

| Accounts Payable (Sundry Creditors) | — | 38,000 |

| GST Input Tax Credit (ITC) Receivable | 9,200 | — |

| GST Output Tax Payable | — | 14,200 |

| Owner’s Capital | — | 2,00,000 |

| Retained Earnings | — | 15,000 |

| Sales Revenue | — | 1,85,000 |

| Cost of Goods Sold (COGS) | 95,000 | — |

| Salaries Expense | 34,000 | — |

| Rent Expense | 18,000 | — |

| Utilities Expense | 5,000 | — |

| Total | 4,71,200 | 4,71,200 |

How to View Trial Balance in Tally ERP 9 / Tally Prime

Tally is the most widely used accounting software in India, used by over 2 million businesses, CA firms, Enterprises and SMEs. Knowing how to access and interpret the trial balance in Tally is an essential skill for Indian accountants.

Steps to View Trial Balance in Tally Prime

- Open Tally Prime and select your Company.

- Go to Gateway of Tally → Display More Reports → Trial Balance.

- The report will show all ledger account groups with their closing balances. Debits appear on the left; credits on the right.

- Press F2 to change the date period (e.g., 01-Apr-2024 to 31-Mar-2025 for FY 2024–25).

- Press Enter on any group to drill down and view individual ledger balances within that group.

- Use F12: Configure to show ledger folio numbers, opening balances, and net transactions for the period.

- To export, press Alt+E and choose Excel or PDF format.

Tally Tip: If your trial balance in Tally does not balance, check for any Suspense Account balance under the group Suspense A/c. Tally automatically routes unreconciled entries here, making it easier to identify and fix double-entry errors.

Steps to View Trial Balance in Tally ERP 9

- Go to Gateway of Tally → Display → Trial Balance.

- Press F2 to set the reporting period.

- Use Ctrl+F10 to show ledger-level detail instead of group-level summary.

Trial Balance vs Balance Sheet – Key Differences

A common point of confusion, especially for CA Foundation and CA Inter students in India, is how the trial balance differs from the balance sheet. Here is a direct comparison:

| Parameter | Trial Balance | Balance Sheet |

| Purpose | Verify arithmetical accuracy of ledger | Show the financial position of the business |

| Accounts Included | All accounts — real, nominal, and personal | Only permanent accounts (assets, liabilities, equity) |

| Format | Two columns: Debit and Credit | Two sides: Assets and Liabilities & Equity |

| Statutory Requirement | Not a statutory document; internal use only | Mandatory under Companies Act 2013, Schedule III |

| Income & Expense Accounts | Included | Excluded (closed to P&L before balance sheet) |

| When Prepared | End of accounting period, before financial statements | After the trial balance and P&L statement are finalised |

| Prepared by | Bookkeeper / accountant | Accountant / CA for statutory filing |

Common Errors in Trial Balance – What to Look for and How to Fix Them

A trial balance in accounting does not guarantee error-free book. Certain types of mistakes will not cause a mismatch at all, which is an important limitation to keep in mind. However, many common errors do result in an imbalance and can be systematically tracked down.

Errors that cause an Imbalance (Detectable):

- Arithmetic Errors – Mistakes made while totaling a ledger account or the trial balance in accounting columns themselves.

- Single-sided entry – A debit was recorded without a corresponding credit, or vice versa.

- Transposition errors – Digits are written in the wrong order (e.g., ₹5,400 posted as ₹4,500). The difference between the two column totals is always divisible by 9 in this case, a useful diagnostic clue.

- Wrong column posting – A debit balance placed in the credit column, or the reverse.

Errors that do not cause an Imbalance

- Errors of omission – A transaction is completely left out of the books. Both sides are missing equally, so the balance is unaffected.

- Compensating errors – Two separate mistakes that cancel each other out.

- Errors of principle – A transaction posted to the wrong type of account (e.g., a capital expense recorded as a revenue expense, — critical for correct Income Tax treatment under the Income Tax Act, 1961)

- Commission errors – An entry posted to the correct side but to the wrong account within the same category.

How to fix a Discrepancy:

Then verify that every ledger balance was correctly transferred to the trial balance in accounting. If no arithmetic mistake is found, go back to the original journal entries and re-examine postings one by one. If the gap is divisible by 9, suspect a transposition; if it matches a specific transaction amount exactly, that entry likely has a missing side.

Using a Suspense Account:

When the trial balance in accounting does not agree and you cannot immediately locate the error, open a Suspense Account — a temporary ledger account used to hold the difference. This allows you to proceed with financial statement preparation while the rectification of errors continues. Once all errors are identified, the Suspense Account balance is eliminated through correcting journal entries. This approach is widely used in Indian CA practice and is a key topic in the ICAI CA Foundation & CA Inter syllabus.

Struggling with month-end closing? Let our CA-certified team handle your trial balance,

GST reconciliation, and bookkeeping. Get Your Free Consultation.

People Also Ask:

What is meaning of trial balance in accounting.

A trial balance in accounting statement that presents a list of all the ledger account balances for a particular date. It is ready to determine if the total debits are equal to the total credits. It performs that function for businesses when they are double checking bookkeeping accuracy prior to preparing financial statements.

Which are the three kinds of Trial balance?

There are three types, unadjusted, adjusted and post-closing trial balance. The unadjusted trial balance is done before year-end adjustments and the adjusted trial balance will have accruals and depreciation. Post-closing trial balance is prepared after closing entries and will only include permanent accounts.

Does an agreed trial balance mean the books are free from errors?

No, an agreed trial balance doesn’t prove that the accounts are error free. It simply verifies that the amount of debits and credits are equal. There may still be errors such as omissions, misclassifications, or offsetting errors.

What are the reasons for a trial balance to be out of balance?

A trial balance can be unbalanced due to the arithmetic errors, incorrect posting or due to one sided postings in the journal. Also there can be differences owing to transposition errors. If the difference is divisible by 9, it is likely that a transposition has occurred.

How do I view the trial balance in Tally Prime?

In Tally Prime, go to Gateway of Tally → Display More Reports → Trial Balance. Press F2 to set the date range and Enter to drill into any ledger group. Press Alt+E to export to Excel or PDF. In Tally ERP 9, the path is Gateway of Tally → Display → Trial Balance.

What is the difference between a trial balance and a balance sheet?

A trial balance includes all ledger accounts (including income and expenses) and is used to verify arithmetical accuracy. A balance sheet includes only permanent accounts (assets, liabilities, equity) and is a statutory financial statement under Companies Act 2013 Schedule III. The trial balance is prepared before the balance sheet, and serves as its input.

Conclusion

While the trial balance in accounting is not as complicated as some other financial statements, it is one of the more crucial ones. It ensures that your books are correct prior to figures going into your financial statements. For Indian businesses, it also serves as a critical checkpoint before GST return filing, statutory audit, and MCA filings under the Companies Act 2013.

Whether you are preparing an unadjusted, adjusted, or post-closing trial balance — or viewing it via Tally ERP / Tally Prime — accuracy and consistency are non-negotiable. With Corient Business Solutions, we assist businesses with periodic bookkeeping, ledger reconciliation, and period-end closing, helping you identify errors early and maintain dependable financial records.