GST 2.0 is India’s restructured Goods and Services Tax regime, effective 22 September 2025. It replaces the four-slab system with two core rates — 5% and 18% — plus a 40% rate for sin and luxury goods and a nil rate for most essentials. This guide explains what it means for enterprise compliance, and when to bring in a Compliance Specialist.

What changed at a glance

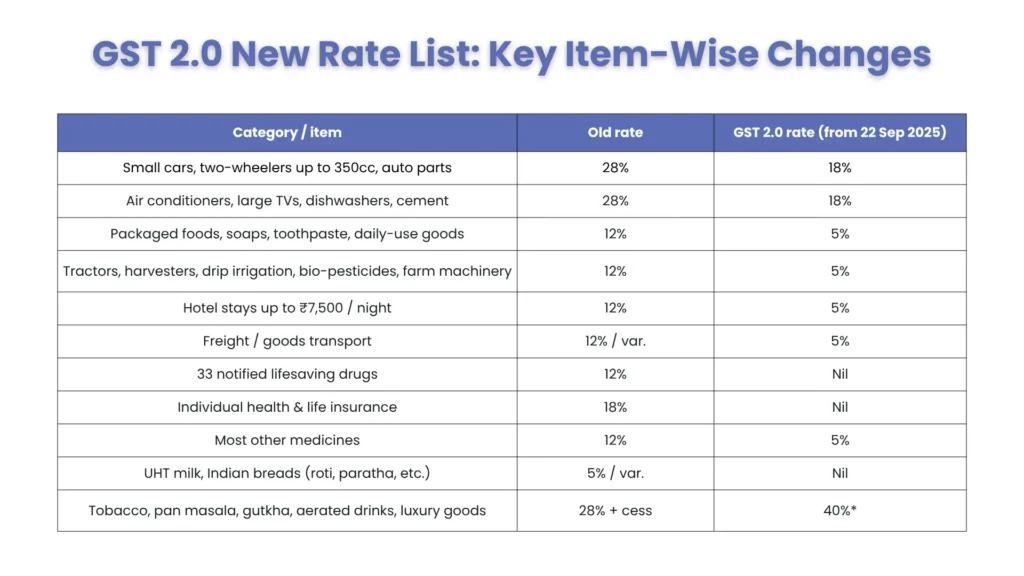

- Four slabs (5% / 12% / 18% / 28%) collapse into two core slabs: 5% and 18%

- New 40% rate for sin / luxury goods (tobacco, pan masala, aerated drinks)

- Nil rate on essentials — 33 notified lifesaving drugs, individual health & life insurance, key foods

- 200 items re-rated: ~90% of items previously rated 28% are now 18%, and ~99% of items previously rated 12% are now 5%.

- GSTAT now operational; hard 30 June 2026 deadline for legacy appeals

GST 2.0 is India’s most significant indirect-tax change since the original Goods and Services Tax launch in 2017. For large enterprises it demands action on ITC recalculation, vendor alignment, ERP updates, and most urgently, the 30 June 2026 GSTAT appeals deadline. The complexity of running these workstreams simultaneously is exactly why many finance teams now bring in a dedicated Compliance Specialist.

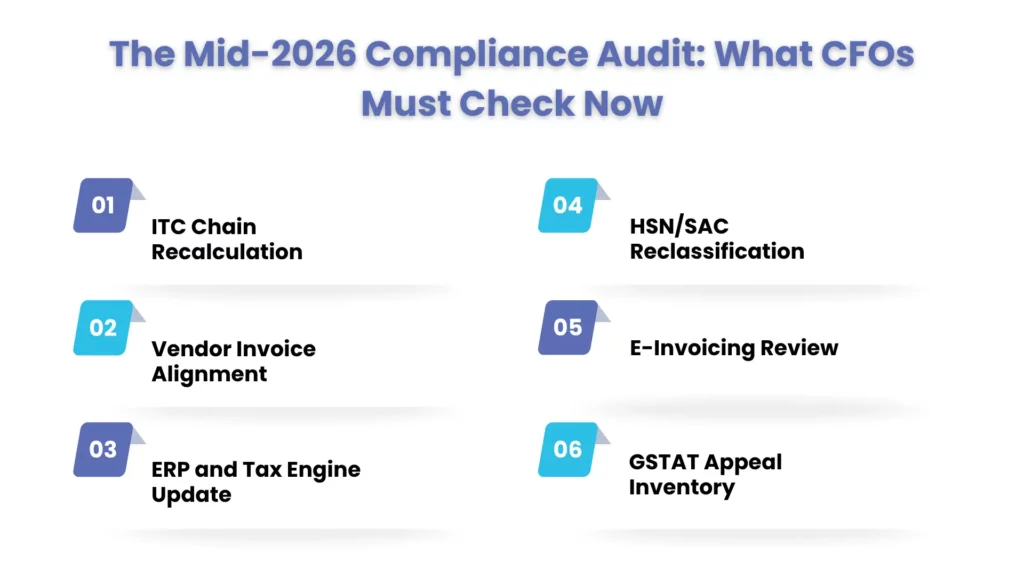

The Mid-2026 Compliance Audit: What CFOs Must Check Now

A Compliance Specialist will typically structure a mid-year audit around six areas.For a working version your team can reuse, see our GST compliance checklist for finance teams.

- ITC Chain Recalculation: Corrected inverted duty structures free credits trapped in manufacturing, textiles, and logistics. Map your input chain against revised slabs and update GSTR-2B reconciliation now .The kind of ongoing close work our record-to-report (R2R) services are built for.

- Vendor Invoice Alignment: Vendors billing at old 12% or 28% create GSTR-2B mismatches. Issue a vendor sweep for Q3–Q4 FY26 invoices before filing deadlines.a disciplined procure-to-pay (P2P) process prevents most of them.

- ERP and Tax Engine Update: Tax codes must reflect CBIC notifications of September 17, 2025. Confirm updates are live across all GSTINs.

- HSN/SAC Reclassification: Products at old rates need remapping. Classification errors were the top driver of GST litigation getting this right prevents scrutiny under the new reforms in gst.

- E-Invoicing Review: Businesses above Rs. 10 crores must generate IRNs within 30 days of invoice date. Backdated IRNs are rejected.

GSTAT Appeal Inventory: All adverse First Appellate Authority orders before April 1, 2026 must reach GSTAT by June 30. No extension expected.

GST 2.0 New Rate List: Key Item-Wise Changes

GSTAT Appeals and Dispute Resolution: The June 30 Deadline

The GSTAT was formally launched on 24 September 2025 and began hearing cases in February 2026. The transitional appeal deadline is set by Notification S.O. 4220(E), dated 17 September 2025.It ends eight years without a dedicated second-tier appellate forum. Over 5 lakh appeals representing more than ₹1 lakh crore in disputed tax are eligible. Appeals are filed online in Form GST APL-05 on the GSTAT e-filing portal.

30 June 2026 is the transitional deadline for orders communicated before 1 April 2026. The government has signaled no further extension of this window. While Section 112 contains a limited, discretionary condonation provision for delay on sufficient cause, taxpayers should treat 30 June 2026 as a firm cut-off and not rely on relief.

Pre-deposit under Section 112(8) (amended by Finance (No.2) Act 2024) is 10% of remaining disputed tax capped at Rs. 20 crore per enactment. see the CGST Act on India Code This is additional to the 10% paid under Section 107(6) at first appeal; cumulative total is 20%. A common error is computing a fresh 20% at this stage, causing significant overpayment.

Filing workflow (4–6 weeks minimum):

- Audit all adverse orders from July 2017 onwards; priorities by quantum and legal merit

- Compute pre-deposit: 10% of remaining disputed tax per Section 112(8), capped at Rs. 20 crore per enactment

- File Form GST APL-05 with complete documentation at efiling.gstat.gov.in before June 30

Sector-Level Impact for Large Enterprises

The new gst reforms in India do not land equally. Key changes from the 56th GST Council:

| Category | Old GST Rate | GST 2.0 Rate (from 22 Sep 2025) |

| Two-wheelers, small cars, air conditioners, televisions, cement | 28% | 18% |

| Food essentials, soaps, farm machinery, hotel stays up to ₹7,500 | 12% | 5% |

| 33 lifesaving drugs, health insurance, life insurance, education-related services | 12%-18% | 0% (Nil) |

| Tobacco, pan masala, aerated drinks, luxury goods | 28% + cess | 40%* |

ACs, TVs, cement, and auto parts from 28% to 18%. Corrected inverted duty improves margins and conducts a full ITC chain review.

Mid-Year Action Checklist for Finance Teams

Before June 30, 2026:

- File all eligible GSTAT backlog appeals before the hard deadline

- Confirm ERP and billing systems reflect September 22, 2025 CBIC rate changes

- Reconcile GSTR-1 and GSTR-3B for Q3–Q4 FY26 under revised rates

- Correct all vendor invoices still using old 12% or 28% rates

July–September 2026:

- Complete ITC chain review and quantify working capital release for FY27

- Renegotiate logistics contracts to reflect 5% freight GST

- Update HSN/SAC classification mapping across the full product portfolio

- Engage a GST Specialist for sector-specific advisory under GST 2.0

When to Bring in a GST Compliance Specialist, and What to Ask Them

In-house tax teams are built for steady-state compliance, but the current GST environment is anything but steady. Businesses are navigating simultaneous rate restructuring, tight GSTAT deadlines, ITC recalculations, and HSN reclassification, creating unprecedented operational and compliance challenges. Relying solely on internal teams can expose organizations to errors, disputes, and missed opportunities for optimization.

Bringing in a GST Specialist is critical when your organisation faces significant pending GSTAT disputes, operates multi-state supply chains, or needs strategic guidance on pricing, transfer pricing, and working capital implications under GST 2.0. Compliance Specialists help mitigate risk, ensure compliance, and provide actionable insights to adapt smoothly to the new reforms.

Ask before engaging:

- What is your GSTAT-specific track record pre-deposit computation, grounds drafting, and bench appearances?

- Have you mapped September 22, 2025 CBIC rate changes against our sector and full product portfolio?

- How do you handle state-level SGST notification lags under the revised GST reforms in India framework?

Not sure where your GST 2.0 exposure sits?

Get a free compliance health-check across your ITC chain, vendor invoices, ERP rate codes, and appeal inventory, one assessment, clear next steps.

People Also Ask:

What is GST 2.0 and what are the differences as compared with the original GST reform?

GST 2.0 was implemented on 22 September 2025, which reduced the four-slab system in India to primarily 5% and 18%, with 40% levy applied to luxury goods and 0% to essential goods. During the 56th GST Council meeting, they approved these and slashed rates for nearly 200 items. They also establish GSTAT, an extra appellate tribunal, pre-filled returns and quicken ITC refunds. GST was introduced in 2017, when it replaced multiple indirect taxes. With the advent of GST 2.0, it has become easier and more sophisticated.

Is GST a one nation one tax reform and does GST 2.0 fulfil that vision?

Yes. GST merged levies such as excise duty, VAT, and service tax into a single system. GST 2.0 advances the vision by simplifying classification, fixing inverted-duty structures, and giving the system a national appellate body in GSTAT. According to PIB, active GST registrations rose from about 66.5 lakh at launch (2017) to over 1.51 crore as of April 2025.

What if my company misses the 30 June 2026 GSTAT deadline?

For orders communicated on or before 1 April 2026, the transitional GSTAT window closes on 30 June 2026. Over 5 lakh appeals worth more than ₹1 lakh crore in disputed tax are eligible, and the government has indicated no further extension. Treat it as a firm cut-off.

What is the correct pre-deposit for a GSTAT appeal?

Under Section 112(8), as amended by the Finance (No.2) Act 2024, the GSTAT-stage pre-deposit is 10% of remaining disputed tax capped at Rs. 20 crore per enactment for CGST and SGST separately. This is additional to the 10% paid at first appeal under Section 107(6); the cumulative total is 20%. A common error is computing a fresh 20% at this stage, causing significant working capital overpayment.

Do GST 2.0 changes require ERP and e-invoicing updates?

Yes, Invoices at old 12% or 28% rates after September 22, 2025 create GSTR mismatches and ITC reversal risk. ERP tax codes must reflect CBIC notifications of September 17, 2025. Businesses above Rs. 10 crore AATO must generate IRNs within 30 days of invoice date backdated IRNs are rejected. Reconcile all FY26 Q3–Q4 filings only after confirming all system updates are live.

When should I hire a GST Compliance Specialist?

A Compliance Specialist adds value when you have pending GSTAT disputes, operate across multiple states, or need pricing and working-capital decisions modelled under the new rates. For tribunal matters specifically, choose a GST Expert with a documented GSTAT track record rather than general advisory support.

Conclusion

Does a “one nation, one tax” reform exist with GST? It was conceived to be just that and GST 2.0 makes it more true to the desired concept. The convergence of fewer tax slabs, establishment of the GST appellate tribunal and essential items being nil rated, are some vital measures that have been taken towards simplifying India’s tax regime. GST collections reached a record ₹22.08 lakh crore in FY 2024-25, a 9.4% year-on-year rise, highlighting the success of the implementation of the Goods and Services Tax.

The changes present opportunities and challenges to businesses. By working with a Compliance Specialist to preemptively file GSTAT appeals, modify input tax credit claims, and revise supplier agreements and ERPs before the filing deadline, companies can minimize future legal issues and maximize operations. Corient Business Solutions offers GST 2.0 advisory, compliance assistance, and tax planning solutions to help your business through this transition.