Every month, your finance team files returns, reconciles figures, and ticks off the GST calendar. But staying busy with GST is not the same as being GST compliant.

Established businesses with dedicated finance departments and GST software in place are still receiving compliance notices, not because they are negligent, but because the compliance landscape in 2026 has fundamentally changed.

ITC mismatches, IMS Zero Mismatch Policy, tightened e-invoicing mandates, and stricter reconciliation requirements have raised the bar for what truly being GST compliant means today.

So what went wrong? And more importantly, is your organisation quietly accumulating the same risks?

What It Truly Means to Be GST Compliant in 2026

When most finance professionals hear “GST compliant,” they picture return filing on time. That’s understandable, it’s the most visible obligation. But for businesses with turnover above ₹5 crore, staying GST compliant in 2026 covers a significantly broader scope:

- Accurate preparation and timely filing of GSTR-1, GSTR-3B, GSTR-9, and GSTR-9C

- Correct computation of CGST, SGST, IGST, and applicable cess

- Disciplined ITC management, claiming only eligible credits and reversing where required under Sections 16 and 17 of the CGST Act

- Maintaining complete records: invoices, credit notes, e-way bills, and reconciliation statements under Section 35

- Generating e-invoices with valid IRNs through the IRP portal for all B2B transactions

- Responding correctly and within deadline to GST notices, SCNs, and audit queries

For multi-GSTIN organisations, each of these obligations multiplies. An ITC error worth ₹50,000 for a small business can translate to ₹5 crore for a large enterprise operating across 15–20 GSTINs. The arithmetic of non-compliance scales fast.

The 2026 Game Changer: IMS and the Zero Mismatch Policy

If there’s one development that has fundamentally altered the stakes for remaining GST compliant in 2026, it’s the Invoice Management System (IMS) and its Zero Mismatch Policy.

Effective April 2026, the GSTN portal will hard-block the filing of GSTR-3B if the ITC claimed in your return exceeds what is reflected in your GSTR-2B. This is not a warning. It is a system-level block, your return simply cannot be filed until the discrepancy is resolved.

What this means practically:

- Your finance team must reconcile, approve, or reject vendor invoices in IMS on at least a weekly basis, see our GST Compliance Checklist for FY 2026-27 for the full monthly action list

- Any supplier who hasn’t uploaded their GSTR-1 on time will directly prevent you from filing on time

- Backlogs from prior years compound the problem, pending GSTR-9 or GSTR-9C from previous years will also block your current year GSTR-3B filing

The old workaround of claiming ITC based on books and settling differences later is gone. Vendor performance is now directly your compliance risk.

The Six GST Errors That Prevent You From Being GST Compliant

1.ITC Mismatch Between GSTR-2B and GSTR-3B

This is the single largest source of notices among large taxpayers and a primary reason enterprises struggle to stay compliant. When a supplier fails to upload an invoice in their GSTR-1, it disappears from your GSTR-2B. If your team claims ITC in GSTR-3B anyway, based on the physical invoice in your books — the department will issue a notice under Section 61 or raise a demand under Sections 73 or 74.

The fix: Never file GSTR-3B without first reconciling it against GSTR-2B. Build the reconciliation into the filing workflow, not as a separate post-filing exercise.

2.Claiming Blocked Credits Under Section 17(5)

ITC on motor vehicles used for non-business purposes, food and beverages, club memberships, and construction works that are capitalised in the books is explicitly blocked under Section 17(5). This shows up consistently in GST audits because the credit is visible in GSTR-2B but not legally claimable.

The fix: Configure your ERP to flag these categories automatically and route them for manual review before any ITC claim is posted.

3.Skipping ITC Reversal for Exempt Supplies

If your business makes both taxable and exempt supplies, you are required to reverse a proportionate share of common ITC under Rules 42 and 43 of the CGST Rules. Many large organisations — particularly in real estate, banking, and manufacturing — routinely underestimate or skip this reversal.

The fix: Build the Rule 42/43 calculation into your quarterly GST audit process, not just at year-end.

4.E-Invoicing Gaps

An invoice without a valid IRN is not legally recognised under GST. It exposes both you and your buyer — neither party can claim ITC on it. For organisations with AATO above ₹5 crore, every B2B invoice must be generated through the IRP portal in real-time. From 2026, businesses with AATO above ₹10 crore cannot raise IRNs more than 30 days after the invoice date.

The fix: Integrate your billing system directly with the IRP. Manual IRN generation processes are a compliance liability at scale. Learn how AP automation integrates e-invoicing into your payables workflow.

5.Place of Supply Errors

Getting the place of supply wrong, particularly in service transactions and interstate deals — means tax is being paid to the wrong government. Correcting this requires amendments, refunds, and sometimes litigation. It’s a surprisingly common error in logistics, IT services, and construction.

The fix: Document and periodically review your place of supply determination logic, especially after new contracts or service models.

6.Inconsistency Between GSTR-1 and GSTR-3B

Any mismatch between what you’ve reported in GSTR-1 (outward supplies) and what’s reflected in GSTR-3B (your self-assessed summary) triggers an automated DRC-01B notice from GSTN. Credit notes and amendments are a common source of such mismatches.

The fix: Treat GSTR-1 and GSTR-3B as twin filings, reconcile them before submitting either.

Understanding GST Grievances, Complaints, and Notices: What Each One Means

Not all communications from the GST department carry equal weight. Finance teams that confuse a GST grievance with a Show Cause Notice often either overreact or underreact — both of which create problems. Here’s how to distinguish them.

GST Grievance vs. Show Cause Notice

A GST grievance is a discrepancy flag raised by GSTN based on mismatches found in your filed returns, typically in GSTR-1, GSTR-3B, or your ITC claims. It is an invitation to clarify, not yet a demand. Businesses that are GST compliant and have clean reconciliation records can typically resolve a GST grievance quickly with supporting documentation.

A Show Cause Notice (SCN) under Sections 73 or 74, by contrast, is a formal legal document initiating a demand proceeding. It requires a detailed written response within the stipulated timeframe. Ignoring it or missing the response deadline results in an ex parte demand order, and potentially, property seizure.

How to File a GST Complaint Online

If your business is on the receiving end of fraudulent invoicing, fake ITC claims by counterparties, or supplier misconduct, you can file a GST complaint online through the official GST complaint portal at grievance.gst.gov.in . The platform allows taxpayers to:

- Lodge a GST fraud complaint against suppliers issuing fake invoices

- Raise a GST grievance related to technical issues on the GSTN portal

- Report suspected GST fraud by unregistered entities or fly-by-night operators

For matters related to GST fraud complaints, such as a vendor fraudulently claiming ITC or generating fake e-invoices against your GSTIN, you can also reach the GST helpdesk at the GST complaint number: 1800-103-4786 (toll-free), available on working days. Serious fraud cases may additionally be referred to the Directorate General of GST Intelligence (DGGI).

Why GST Fraud Complaints Matter for Large Enterprises

Large organisations are increasingly targeted by fraudulent vendors who generate fake invoices to pass on bogus ITC. If a fraudulent invoice appears in your GSTR-2B, you may be inadvertently processing ineligible credit. A proactive GST fraud complaint filed through the GST complaint portal protects your organisation and creates a formal trail that can be referenced if the department later questions your ITC claims.

Being GST compliant is not just about your own filings — it also means actively monitoring for fraud in your supply chain.

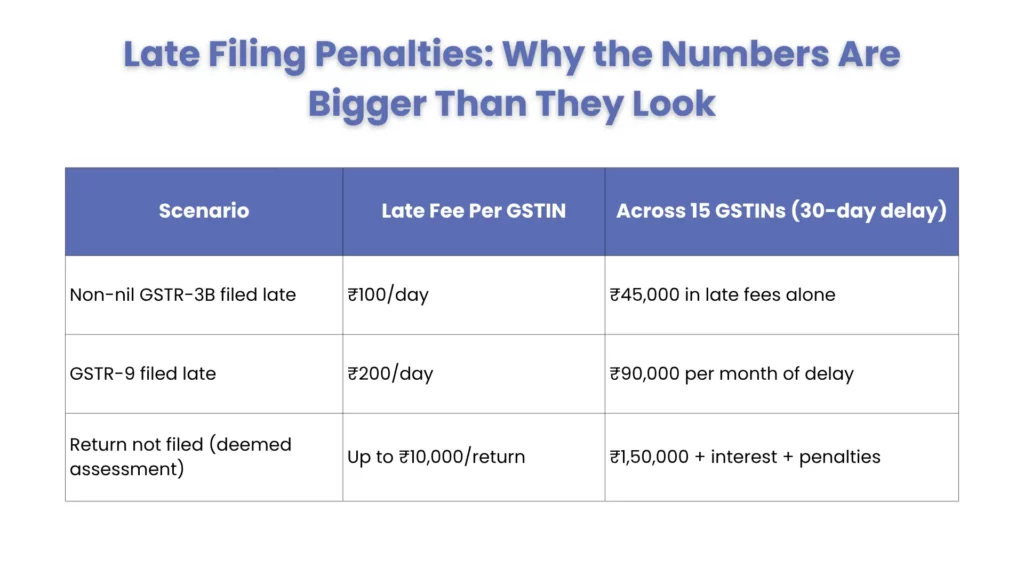

Late Filing Penalties: Why the Numbers Are Bigger Than They Look

Late fees sound manageable in isolation. At ₹100 per day per GSTIN for a non-nil return, it doesn’t feel alarming. But consider the enterprise reality:

And then there’s interest. Under Section 50, unpaid GST attracts 18% per annum from the original due date. A monthly GST liability of ₹5 crore delayed by just 15 days costs approximately ₹3.7 lakh in interest, before any late fees.

There are also indirect costs: persistent late filings lower your GST compliance rating on the GSTN portal, which increasingly affects vendor due diligence and government procurement eligibility. In extreme cases, non-filing can trigger registration cancellation under Section 29(2), disrupting invoicing, ITC chains, and banking covenants simultaneously.

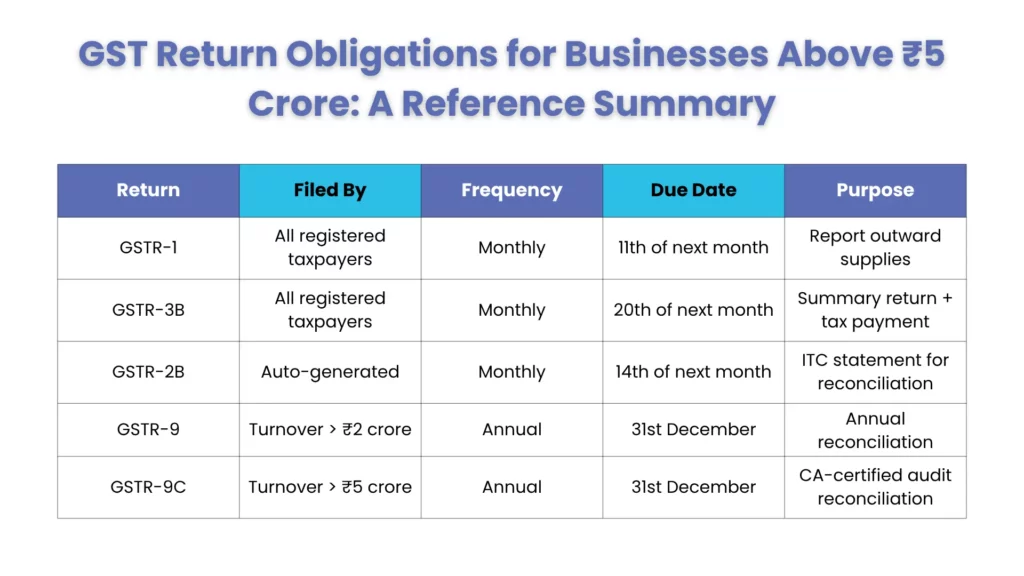

GST Return Obligations for Businesses Above ₹5 Crore: A Reference Summary

A few things worth flagging for 2026:

GSTR-1 errors are costly and permanent. Wrong GSTINs, incorrect HSN/SAC codes, or wrong taxable values cannot be corrected retroactively for the same period. Businesses with AATO above ₹5 crore must now report 6-digit HSN/SAC codes on all invoices, non-compliance means the invoice will be rejected at the IRP portal.

GSTR-9C demands early action. The certification by a Chartered Accountant or Cost Accountant takes time. Starting GSTR-9C preparation in Q3 of the financial year rather than waiting until December significantly reduces the risk of last-minute errors and missed deadlines.

QRMP does not apply to you. Quarterly filing is available only to businesses below ₹5 crore. If you’re above that threshold, monthly filing is mandatory, no exceptions.

Building a GST Compliant Framework That Actually Holds Up

Reactive compliance, filing when due, responding to notices when they arrive, isn’t sufficient at enterprise scale. Organisations that are consistently GST compliant build the following into their operations:

A master compliance calendar tied to GSTINs

Every GSTIN, every return, every due date, and every responsible owner should be mapped and automated for reminders. An organisation with 20 GSTINs generates over 300 return obligations per year. Without systemisation, things slip.

A supplier performance program

ITC hygiene begins with your vendors, not with your reconciliation team. Include contractual clauses for timely GSTR-1 filing. Flag underperforming suppliers in GSTR-2B early and follow up proactively before the filing window closes.

ERP-integrated reconciliation

Manual reconciliation at enterprise scale is error-prone and slow. GST-enabled ERP solutions, whether SAP GST, Tally Prime, ClearTax GST, or others — can automate the GSTR-2B reconciliation, surface mismatches early, and generate the IMS action queue for vendor invoice approvals.

Quarterly internal GST audits.

Don’t wait for the annual return cycle to identify blocked credit claims, ITC reversal gaps, or place of supply errors. A quarterly internal review catches these while corrections are still practical.

A GST grievance and notice response protocol.

When a GST grievance notice or SCN arrives, the response window is typically 30 days. A documented escalation path — from the GST compliance team to finance leadership to external tax counsel, ensures you’re not scrambling. Missed response deadlines convert queries into confirmed demands.

Advance Rulings for uncertain positions.

Under Section 97 of the CGST Act, businesses can seek a binding ruling on classification, valuation, or ITC eligibility. This is underutilised by large enterprises and significantly reduces the risk of a future demand on ambiguous transactions.

A Quick Note on GST Demand Timelines

The GST department can issue a demand notice up to three years from the due date of the annual return for the relevant period, assuming no fraud. If fraud or wilful misstatement is established, that window extends to five years.

This means compliance decisions made today can come back as demands well into the latter part of the decade. The cost of a proactive compliance programe is almost always lower than the cost of a contested demand three years later.

People Also Ask:

What is the e-invoicing threshold in 2026?

E-invoicing is mandatory for all B2B transactions in businesses with AATO above ₹5 crore. Invoices must carry a valid IRN generated in real-time through the IRP. Businesses with AATO above ₹10 crore cannot raise backdated IRNs beyond 30 days from the invoice date.

Can ITC be claimed if the supplier hasn’t filed GSTR-1?

No. Under Section 16(2)(aa) of the CGST Act, ITC is allowed only to the extent it appears in GSTR-2B. From April 2026, the IMS Zero Mismatch Policy hard-blocks GSTR-3B filing if claimed ITC exceeds GSTR-2B figures.

What’s the difference between GSTR-9 and GSTR-9C?

GSTR-9 is the annual return summarising supplies, ITC, and taxes paid — mandatory for turnover above ₹2 crore. GSTR-9C is a reconciliation statement certified by a CA or Cost Accountant, required for turnover above ₹5 crore. Pending annual returns from prior years will block GSTR-3B filing from April 2026.

How is a GST grievance different from a show cause notice?

A GST grievance is a discrepancy flag raised by GSTN, typically related to return mismatches or ITC claims, it is a clarification request, not a demand. A Show Cause Notice (SCN) under Sections 73 or 74 is a formal demand proceeding. Non-response to an SCN leads to an ex parte demand order and potential property seizure.

How do I file a complaint on the GST complaint portal?

You can raise a GST complaint online at grievance.gst.gov.in. For reporting GST fraud such as fake invoicing or bogus ITC claims, use the same GST complaint portal or call the GST complaint number 1800-103-4786. Serious fraud cases can be escalated to the DGGI.

How far back can the GST department raise a demand?

Three years from the due date of the annual return, where no fraud is involved. Five years if fraud or wilful misstatement is established.

The Bottom Line: Final Thought: Being GST Compliant Is a Working Capital Decision

It’s easy to frame GST compliance as a legal and regulatory function. But for large enterprises in 2026, being GST compliant is equally a working capital and cash flow decision.

Blocked ITC due to vendor mismatches locks up cash. Late fees and interest are direct bottom-line costs. A poor compliance rating complicates supplier negotiations and procurement bids. Registration suspension disrupts operations across every business unit.

Finance leaders who treat staying GST compliant as a strategic function, with the same rigour applied to financial reporting or internal audit, consistently outperform those who treat it as a back-office filing exercise. The infrastructure investment pays for itself quickly, usually within the first notice it helps you avoid.

Managing GST compliance across multiple GSTINs, reconciling ITC at scale, and staying ahead of evolving GSTN requirements is a full-time responsibility. At Corient Business Solutions, we support large enterprises with end-to-end GST compliance management, from return preparation and reconciliation to audit support and notice response.